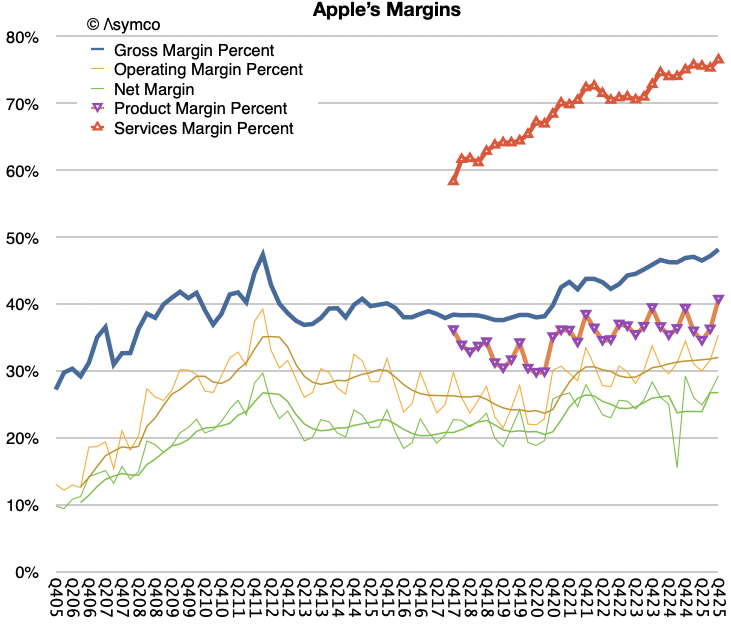

Apple announced a gross margin of 48.2% for the last quarter, exceeding the high end of management's guidance and increasing by one hundred basis points sequentially, according to a report from asymco.com. This performance, which management attributed to "favorable mix and leverage," signals the company is operating at its highest gross and net margins in its history.

Product gross margin specifically reached 40.7%, showing a sequential increase of four hundred fifty basis points, driven by strong product cycles and favorable component pricing dynamics. The Services division also demonstrated strength, delivering a gross margin of 76.5%, up one hundred twenty basis points sequentially, as reported by the firm.

During the earnings call, which the source termed a "Margin Call," analysts pressed executives on component supply, particularly regarding memory costs, which were a central focus. Chief Executive Tim Cook confirmed constraints existed in securing advanced silicon nodes, but stated memory costs had only a minimal impact on the December quarter results.

Executives provided guidance projecting the next quarter's gross margin to reside between 48% and 49%, maintaining the high level despite anticipated, though comprehended, memory cost impacts in the following period. This forward guidance suggests Apple anticipates continued favorable dynamics even with potential headwinds.

Analysts remained visibly surprised by the margin strength given prevailing industry narratives concerning component inflation. One analyst noted his shock at the 48% to 49% guidance, questioning if the growth was driven disproportionately by higher-margin services revenue.

Executives further detailed that investments in proprietary silicon, such as custom SoCs and modems, contribute strategically to product differentiation while also positively impacting gross margin over time. This vertical integration provides both roadmap control and cost-saving opportunities, according to management.

The persistent commentary from financial observers suggests an assumption that Apple will inevitably face margin compression from memory supply issues, despite management's assurances. The evidence, however, points toward Apple maintaining significant supply chain leverage due to its scale and engineering capabilities.

Ultimately, Apple’s ability to consistently expand margins while navigating complex supply constraints highlights its structural advantages within the technology ecosystem. This sustained performance suggests that the company's vertical integration and high-demand product cycles continue to outweigh external economic pressures.